Excise guidelines for the alcohol industry

-

This document incorporates revisions made since original publication. View its history and amending notices, if applicable.

07 REMISSIONS, REFUNDS, DRAWBACKS & EXEMPTIONS

7.3.6 WHEN ARE EXCISABLE ALCOHOL PRODUCTS EXEMPT FROM EXCISE DUTY? |

7.1 PURPOSE

This chapter deals with:

- when you can apply for a remission, refund or drawback

- what happens if you are overpaid a refund or drawback

- when alcohol products are exempt from excise duty

- who can access alcohol products free of excise duty

- how to apply for a remission, refund or drawback, and

- penalties that can apply to offences in relation to remissions, refunds, drawbacks and exemptions.

7.2 INTRODUCTION

A remission of excise duty extinguishes the liability for duty that was created at the point of manufacture.

A refund is the repayment of duty that has already been paid.

A drawback is a repayment of duty already paid. It is similar to a refund, but applies where duty-paid goods are exported.

In some circumstances the duty you pay on goods may be subject to a complete or partial refund or drawback. [165]

7.3 POLICY AND PRACTICE

7.3.1 WHEN CAN I APPLY FOR A REMISSION OF EXCISE DUTY?

You can apply for a remission of excise duty payable on your excisable alcohol products if the following circumstances apply while the goods are subject to excise control :

Where the alcohol products have deteriorated or been damaged, pillaged, lost or destroyed, or become unfit for human consumption

[166]|

| 'Pillaged' means to strip of money or goods by open violence, as in war; plunder. [167] This does not cover simple cases of theft. |

|

| 'Lost' in this context does not simply mean can ' t be found. For example a tank may spring a leak and it is known that the alcohol has drained away. The alcohol has been lost. |

Brewers no longer need to apply for a remission to destroy beer they manufacture that is damaged or not fit for consumption if:

- they destroy less than (or equal to) 125 litres of pure alcohol in a quarterly period

- the goods are under our control, and

- they haven't paid excise duty on them.

Brewers must keep detailed record of the goods they destroyed and be able to present them to us upon request.

|

| For more information about payment of duty see Chapter 6 - Payment of duty . |

|

| The approval of a remission does not constitute permission to remove goods from an excise establishment prior to destruction. Off-site destructions require a movement permission from us. |

|

| For more information refer to Chapter 5 - Movement permissions . |

Example 7A

A pallet of bottled beer is dropped inside the brewery's bond store, damaging the contents. The brewery applies for a remission of duty on the damaged goods. On receiving approval, the brewery destroys the damaged goods and retains records of the destruction.

RTDs containing milk products remain unsold in a manufacturer's licensed premises and have deteriorated to a point where they are unfit for human consumption. The manufacturer applies for a remission of duty on the RTDs. On receiving approval, the manufacturer destroys the unsaleable stock and retains records of the destruction.

Where the goods are not worth the amount of excise duty payable on the goods if delivered into home consumption

[168]Example 7B

A brewery produces an excess of product for export to Japan. Due to the labelling the excess product cannot be sold in Australia.

The brewery applies for a remission on the basis that the amount of duty payable on the leftover stock exceeds the value of the stock, because the stock has no commercial value.

On receiving approval, the brewery destroys the unsaleable stock and retains records of the destruction.

The excisable alcohol products are for sale to diplomatic or consular missions and the goods are to be delivered under your PSP.

[169]Example 7C

A manufacturer receives an order from a diplomatic mission for beer, for official use. The manufacturer delivers the beer, into the Australian domestic market (to the diplomatic mission), under the terms of their PSP. (The terms of the PSP may require the manufacturer to submit an Excise remission (NAT 4289) to us, after delivery of the beer.)

When are excisable alcohol products subject to remission without application?

Under the 'excise remission scheme for manufacturers of alcoholic beverages' (Remission Scheme), licensed manufacturers may be eligible for a full remission of their liability to pay excise duty on beer, spirits or other excisable beverages they have manufactured and entered into home consumption on and after 1 July 2021, up to a maximum of $350,000 per year.

|

| For more information about the Remission Scheme see paragraph 7.3.3 . |

You can supply excisable alcohol products exempt from duty when they are for official use but not for trade by [170] :

- the Governor-General or any member of the Governor-General's family

- State Governors or any member of a State Governor's family

- the Australian American Foundation (Australian-American Fulbright Commission)

- the Government of another country, under an agreement between that Government and the Australian Government

- persons covered by a Status of Forces Agreement, and

- the personnel of sea-going vessels of the Royal Australian Navy (RAN) or Australian Military Forces (AMF) (see below for more detail).

|

| If you are not certain whether someone falls into one of these categories, you should contact us by phone on 1300 137 290 . |

Some restrictions apply to alcohol products for the RAN and AMF:

- The goods must be for consumption by the personnel of sea-going vessels of the RAN or the AMF when:

- such vessels are in full commission, and

- the products are consumed on such vessels [171]

- Only certain excisable alcoholic products are eligible for this concession, including:

- ale, porter and other beer

- brandy

- whisky

- rum

- gin, and

- liqueurs.

|

| RTDs (for example pre-mixed rum and cola or other mixers in bottles/cans) do not qualify for this concession. |

To supply alcohol products under these circumstances, you must first ensure the receiver meets the relevant criteria. For example, you should only accept orders, stating that the goods are for official use, on the official stationery, or official order, of eligible people or organisations. You must keep a copy of this documentation.

Brewers can destroy beer they manufactured that is damaged or not fit for consumption for up to 125 litres of pure alcohol in a quarterly period.

|

| You do not have to apply for a remission in these circumstances. |

7.3.2 WHEN CAN I APPLY FOR A REFUND OF EXCISE DUTY?

You can apply for a refund of excise duty paid on excisable alcohol products if the following circumstances apply:

- Duty has been paid on excisable alcohol products, however it is later found that, while the goods were subject to excise control (that is, while they were at the licensed site), they deteriorated or were damaged, pillaged, lost or destroyed, or become unfit for human consumption. [172]

Example 7D

A manufacturer delivers RTDs into the Australian domestic market and pays duty under its PSP. After the product has gone into the market, it is found that, due to a fault in the packaging, the product is unfit for human consumption. It is evident that the product was unfit for consumption at the time the goods were subject to excise control.

The manufacturer applies for a refund of duty on the RTDs.

Example 7E

A storage licence holder, who does not have a PSP, pays the excise duty on alcohol products in accordance with a pre-payment return. They receive a Delivery authority . Before the alcohol products are removed from the licensed premises, they are destroyed by fire. As the alcohol products were still subject to excise control when they were destroyed, the licence holder can apply for a refund of duty on the alcohol products.

- Duty-paid alcohol products, while the goods are subject to excise control, are not worth the amount of excise duty paid. [173]

Example 7F

A storage licence holder who does not have a PSP pays the excise duty on RTDs in accordance with a pre-payment return. They receive a Delivery authority . Before the RTDs are removed from the licensed premises they become unsaleable, due to changed packaging requirements, and they cannot be sold (but are not unfit for human consumption). As the RTDs were still subject to excise control when they became unsaleable, the licence holder can apply for a refund of duty on the RTDs.

- Duty has been paid through manifest error of fact or patent misconception of the law. [174]

This circumstance applies to an error that is evident, obvious or apparent and also in situations where duty has been paid on goods entering the Australian domestic market that are not excisable. In both cases a refund of the duty paid would be payable.

Example 7G

A manufacturer delivers wine based RTDs that are 11% alcohol by volume into the Australian domestic market. The goods were entered under subitem 3.2 on the excise return as 'other excisable beverages exceeding 10% alcohol by volume'. The goods fit the description of wine based products and are subject to WET, but are not excisable.

The manufacturer applies for a refund of the duty paid through patent misconception of the law and pays WET on the goods.

- Duty-paid goods have been taken up as ship's stores or aircraft's stores. [175]

Ship's stores on overseas ships and aircraft's stores on international flights are not subject to excise duty. Where duty has been paid and the excisable alcohol products are subsequently re-directed for use on ships or aircraft travelling overseas, this refund circumstance may apply.

- From April 2015, duty paid goods that haven ' t been used are returned to licensed premises, or to a person authorised by the manufacturer of the goods to receive them on their behalf, and the goods are destroyed, or are subjected to further manufacture or production. [176]

The goods do not have to be returned to the licensed premises of the original manufacturer. The law provides that they may be returned to premises are licensed under section 39A of the Excise Act or to a person authorised by the manufacturer (for example, a destruction facility).

Example 7H

A retailer has cartons of cream based RTDs that have passed their use by date. The retailer returns them to the licensed manufacturer where they are destroyed. The manufacturer claims a refund of the duty that was paid on the goods when they were entered for home consumption.

- Duty paid goods are sold in the following circumstances

[177]

:

- for the official use of diplomatic or consular staff of foreign countries

- for use by the Government of another country, under an agreement between that Government and the Australian Government and not for trade

- for the official use of a foreign country under a Status of Forces Agreement with the Australian Government and not for re-sale, or

- for the official use of an international organisation, or personal use of the holder of a high office of an international organisation, to which the International Organisations (Privileges and Immunities) Act 1963

- Under the 'excise refund scheme for alcohol manufacturers' (Refund Scheme), licensed manufacturers of beer, spirits and other excisable beverages may be eligible to claim a refund of 60% of the excise duty they have paid on beer, spirits or other excisable beverages they have manufactured, up to a maximum of $100,000 per year.

|

| For more information about the Refund Scheme see paragraph 7.3.3 . |

7.3.3 AM I ELIGIBLE FOR A REMISSION UNDER THE EXCISE REMISSION SCHEME FOR MANUFACTURERS OF ALCOHOLIC BEVERAGES?

The 'Excise remission scheme for manufacturers of alcoholic beverages' ( Remission Scheme ) applies to licensed alcohol manufacturers who have a liability to pay excise duty on the manufacture of an alcoholic beverage that has entered home consumption on or after 1 July 2021 .

The Remission Scheme replaces the 'Excise refund scheme for alcohol manufacturers' ( Refund Scheme ), which itself replaced the 'Brewery refund scheme'. 179

The Refund Scheme applies to licensed alcohol manufacturers who have:

- manufactured and paid excise duty on an alcoholic beverage entered for home consumption prior to 1 July 2021, or

- entered an alcoholic beverage for home consumption in June 2021 and paid the duty on or after 1 July 2021.

Which scheme applies to you?

Timing | Applicable scheme | Entitlement |

Goods entered for home consumption and duty paid by 30 June 2021 | Refund Scheme | 60% of the duty paid Maximum refund $100,000 per financial year |

Goods entered for home consumption on or after 1 July 2021 | Remission Scheme | 100% remission of duty Maximum remission $350,000 per financial year |

Goods entered for home consumption from 1 June to 30 June 2021 and duty paid on or after 1 July 2021 | Transitional provisions apply | Refund of 60% of the duty paid Maximum refund of $8,333 |

Goods entered for home consumption prior to 1 June 2021 and duty paid on or after 1 July 2021 | No applicable scheme | No entitlement |

How much is the remission or refund?

Under the Remission Scheme, from 1 July 2021, you (an alcohol manufacturer) are entitled to receive an automatic remission of 100% of your excise duty liability for one or multiple kinds of eligible alcoholic beverages you manufacture. The maximum remission is $350,000 for each financial year. 180

For excise duty paid prior to 1 July 2021, the Refund Scheme applies. On application, you are entitled to a refund of 60% of the excise duty you paid for one or multiple kinds of eligible alcoholic beverages you manufacture. The maximum refund is $100,000 for each financial year. 181

Transitional rules

Transitional rules apply where excise duty has been paid on or after 1 July 2021 for alcoholic beverages that have been entered for home consumption between 1 June 2021 to 30 June 2021. In this circumstance, on application, you are entitled to claim a refund of 60% of the duty paid up to a maximum of $8,333. 182

Part-year eligible manufacturers

Your maximum remission or refund is pro-rated if you commenced being an eligible alcohol manufacturer part-way through a financial year. The amount is calculated using the following formula.

For remission 183 :

| $350,000 × eligible days |

| 365 |

For refund 184 :

| $100,000 × eligible days |

| 365 |

Where:

Eligible days is the total days calculated from the day the entity started as an alcohol manufacturer until the end of the financial year.

When will you receive your remission or refund?

Remission Scheme

A remission of your liability to pay excise duty on eligible alcoholic beverages you manufacture occurs automatically once it has been entered into home consumption. You do not need to apply to receive the remission. However, you will need to specify on your excise return the alcoholic beverage to which the remission applies and the amount of remission applicable.

If you mistakenly pay your liability to excise duty on an eligible alcoholic beverage that would otherwise qualify for remission under the Remission Scheme, you can apply for a refund of that amount. 185 You must claim the refund within 12 months after the day the excise duty was paid. 185A The refunded amount forms part of your maximum entitlement of $350,000 for the year in which the goods to which the refund relates were entered for home consumption. 185B

Refund Scheme

Your entitlement to a refund under the Refund Scheme arises in the financial year in which you pay the excise duty on the alcoholic beverage. Where you entered eligible alcoholic beverages for home consumption and paid excise duty on or before 30 June 2021 , you can apply for a refund up to the maximum entitlement of $100,000 for that financial year. You must apply for the refund within 12 months after the day you paid the excise duty, otherwise your entitlement will be lost.

If you entered eligible alcoholic beverages for home consumption prior to 1 June 2021 but did not pay the excise duty on or before 30 June 2021 , your entitlement to a refund under the Refund Scheme has ceased and you are not entitled to a remission under the Remission Scheme for those alcoholic beverages. 185C

As part of the transitional arrangements to the Remission Scheme, where eligible alcoholic beverages entered home consumption in the period from 1 June 2021 to 30 June 2021 , and you paid the excise duty on or after 1 July 2021 , you are entitled to a refund of 60% of the excise duty paid. The maximum refund is $8,333. You will have 12 months from the day after payment of the excise duty to apply for a refund, otherwise your entitlement will be lost. The refund of $8,333 in this circumstance does not count toward your maximum entitlement of $350,000 per year under the Remission Scheme.

Eligibility under the excise remission or refund scheme for alcohol manufacturers

You will be eligible if you meet all of the following criteria:

- you are an

alcohol manufacturer

who

- for the Remission Scheme , has a liability to pay excise duty on an alcoholic beverage that you manufactured and entered for home consumption during the financial year

- for the Refund Scheme , has paid excise duty in respect of the financial year on an alcoholic beverage that you manufactured, and

- you are legally and economically independent of any other alcohol manufacturer that has received a remission or refund under the Remission Scheme or Refund Scheme in respect of goods entered during the financial year, and

- you fermented or distilled at least 70% of the alcohol content of the beverage on which you had an excise duty liability (Remission Scheme) or on which you paid excise duty (Refund Scheme), and

- if your remission or refund is in respect of a liability to pay excise duty (Remission Scheme) or excise duty paid (Refund Scheme) on a distilled beverage, you satisfy the 'still ownership test' where required.

These concepts are discussed further.

Eligibility rules explained

(a) Are you an alcohol manufacturer and have you manufactured the alcoholic beverage?

An 'alcohol manufacturer' 185D is defined as 'a licensed manufacturer whose manufacturer licence authorises the manufacture of alcoholic beverages'.

You will only be eligible for:

- a remission under the Remission Scheme, if you have a liability to pay excise duty on an alcoholic beverage you manufactured, and that you entered for home consumption during the financial year, or

- a refund under the Refund Scheme, if you have paid excise duty on an alcoholic beverage you manufactured and that you entered for home consumption during a financial year.

The term 'manufacture' 185E is defined as:

Manufacture includes all processes in the manufacture of excisable goods and, in relation to beer, includes the provision to the public at particular premises of commercial facilities and equipment for use in the production of beer at those premises.

It is clear from this definition that, aside from the specific extension of the definition to encompass the provision of 'brew on premises' facilities to members of the public, 'manufacture' equates to the processes (whether they be physical, mechanical or chemical) involved in the creation of an excisable good. 185F

You will not be considered to have manufactured an alcoholic beverage where you acquire alcoholic beverages from another manufacturer or acquire the business of another manufacturer, including trading stock on hand. To qualify in such circumstances, you would need to undertake further manufacture in respect of the product, such that you produce a product that can be differentiated from the product acquired.

Manufacturing alcoholic beverages under contract

An alcohol manufacturer must manufacture excisable goods at premises specified in its excise manufacturer licence. 185G It is an offence 185H to manufacture excisable goods:

- without an excise manufacturer licence

- at premises that are not listed in your excise manufacturer licence.

It is therefore very important that you have the requisite licence and that it specifies any premises from which you intend to manufacture excisable goods.

Where you engage contractors to manufacture excisable goods, it is a matter of fact and degree whether you can be said to have manufactured the goods.

For the purposes of the Remission Scheme or Refund Scheme, you will be accepted as being the manufacturer of the excisable goods if you engage contractors to manufacture goods where the manufacture occurs under your supervision and direction at your licensed premises.

In contrast, if you engage contractors to manufacture excisable goods at the contractor's premises, you are unlikely to be considered the manufacturer of the goods. Where you enter into a contract with a contractor for the manufacture of excisable goods at the contractor's premises, you will only be considered the manufacturer if:

- you actively participate in the manufacturing process, including providing direction and supervision to the contractor

- you have ultimate control of, and responsibility for, the manufacturing process

- the contractor's premises are also specified in your excise manufacturer licence, and

- under your contract, the contractor merely provides inputs to manufacture (such as use of premises, use of equipment or provision of labour) rather than being contracted to provide you with a quantity of finished goods.

A contractor who is engaged to manufacture excisable goods is likely to be regarded as the manufacturer of excisable goods where the contract is for the manufacture and supply of a quantity of excisable goods and/or where the contractor is not subject to your active participation and control during the manufacturing process. If the contractor is considered to be the licensed excise manufacturer that has manufactured the goods in question, you will have no entitlement to a remission (under the remission scheme) or refund (under the refund scheme) , even where you obtain the goods under bond and enter the goods for home consumption.

Example 7I

We Make Beer Co is a small brewer that holds an excise manufacturer licence. The licence authorises We Make Beer Co to manufacture and store beer at the premises specified on its licence ( licensed premises ).

We Make Beer Co is expanding its product range to include a number of 'ready to drink' fruit flavoured alcoholic beverages that use its beer as the base ( new products ).

Due to the limitations on its premises and facilities, We Make Beer Co is unable to manufacture the new products at its current licensed premises. We Make Beer Co enters into a contract with Frooty Drinx Co, to manufacture the new products on behalf of We Make Beer Co at the premises specified on Frooty Drinx Co's licence.

Under the agreement:

- Frooty Drinx Co will manufacture the new products at its premises using recipes and ingredients supplied by We Make Beer Co.

- Frooty Drinx Co will receive production fees from We Make Beer Co calculated on a 'per litre of finished product' basis.

- We Make Beer Co shall own the ingredients, intermediary goods and finished products at all times as well as the intellectual property associated with the recipes and branding of the new products.

- Frooty Drinx must ensure it has adequate insurance to cover the ingredients, intermediary goods and finished products that it holds on We Make Beer's behalf.

Although We Make Beer Co has supplied the ingredients and recipes for the new products, and owns the inputs, intermediary goods and final products at all stages of the manufacturing process, We Make Beer Co is not actively involved in, nor has the ultimate control over or responsibility for the manufacturing process. Further, the goods are not being manufactured in the licensed premises specified in We Make Beer's excise manufacturer licence. Accordingly, We Make Beer Co is not manufacturing the new product and is ineligible for a remission or a refund.

Frooty Drinx Co did not ferment or distil at least 70% of the alcohol contained in the products (the beer base containing the alcohol was fermented by We Make Beer) and is also ineligible for a remission or refund.

Example 7J

Wishing Well Liquor Co is a distiller. It currently holds an excise manufacturer licence authorising it to manufacture and store spirits and other excisable beverages at premises specified on its licence.

Wishing Well Liquor Co has developed a new range of botanical infused gin ( new products ) and would like to manufacture and sell them on a larger scale than its current production capacity allows. Wishing Well Liquor Co enters into a contract with Large Scale Liquor Co for the manufacture of these new products. The main business of Large Scale Liquor Co is manufacturing fruit infused vodka.

Under the arrangement agreed to by the parties:

- Wishing Well Liquor Co will pay an arm's length monthly payment to Large Scale Liquor Co for the use of its designated factory space, equipment, storage space, and its staff for the manufacture of the new products.

- Wishing Well Liquor Co will use its own ingredients and recipes for the manufacture of the new products.

- Wishing Well Liquor Co owns the products at all times during the entire manufacturing process, including the intellectual property associated with the recipes and the branding of the new products.

- Wishing Well Liquor Co 's head distiller has oversight of the end-to-end manufacturing process. The head distiller will be onsite at all times supervising and directing the staff of Large Scale Liquor Co in manufacturing the new products, as well as bottling and packaging the finished product.

- Wishing Well Liquor Co will be liable for excise duty and will pay duty on these new products.

- Other than providing the resources and facilities to Wishing Well Liquor Co, Large Scale Liquor Co will not participate in the control and management of the manufacture of the new products.

The arrangement is for a fixed period, with an option for Wishing Well Liquor to renew for a further period.

Wishing Well Liquor Co has applied and been granted with an excise manufacturer licence for the premises of Large Scale Liquor Co.

In this case, Wishing Well Liquor Co is directing the manufacturing process, including supervising the staff of Large Scale Liquor Co manufacturing the new products. Wishing Well Liquor Co also has ultimate control of and responsibility for the manufacturing process. The premises where the new products are manufactured are also specified in an excise manufacturer licence held by Wishing Well Liquor Co. As such, Wishing Well Liquor Co is the manufacturer of the new products. Wishing Well Liquor Co will be able to receive the remission or refund if it also satisfies the other eligibility criteria including legal and economic independence.

Note: As Wishing Well Liquor and Large Scale Liquor are dealing with each other on an arm's length basis, and Wishing Well Liquor has the certainty of a fixed term agreement with the option of extending the agreement, its ability to carry on its business is contractually protected and is not dependent on Large Scale Liquor's discretion. Wishing Well Liquor also manufactures and sells its products under its own label, so its marketing of its products is independent from Large Scale Liquor. In the absence of other legal or economic ties between the two manufacturers, Wishing Well Liquor would satisfy the independence test.

(b) When are alcohol manufacturers legally and economically independent?

Where two or more alcohol manufacturers are not 'legally and economically independent', only one alcohol manufacturer in that group is entitled to a remission or refund of excise duty. Once an entity has received a remission or refund for goods entered in a year it may claim further amounts for goods entered in the same year up to the relevant annual limits; other entities in the same group will not be entitled.

In determining if an alcohol manufacturer is 'legally and economically independent' it is necessary to consider whether, through the legal and/or economic connections between manufacturers, they each have capacity to make business decisions independently. The elements of the test must be considered individually - legal independence and economic independence - as well as collectively. This requires a balanced analysis of relevant factors (some of which are set out below) having regard to the facts and circumstances of the case. No one factor is determinative.

Legal independence

Whether one manufacturer is legally independent from another requires consideration of whether one manufacturer is legally capable of exerting influence over the other. This includes where one manufacturer has a controlling interest in the other as evidenced by voting rights or a third party has a controlling interest in both manufacturers.

Factors that are relevant in determining if alcohol manufacturers are legally independent of one another include

- Whether there are

common controlling shareholders

(for companies

only

).

An entity will be considered a controlling shareholder if, as a result of its shareholding in a company, it is capable of influencing the decision making of that company. Where a shareholder has this influence over more than one alcohol manufacturer (that is, a common controlling shareholder), neither alcohol manufacturer will be considered to be legally and economically independent. A shareholding of greater than 50% would generally be a strong indicator that the shareholder can control the actions of a company, depending on the class of shares on issue and the rights attaching to the shares. However, a shareholding that is not greater than 50% may still amount to a degree of control depending on the circumstances. For example, the remaining shareholders may each have small shareholdings or there may be different classes of shares whereby one shareholder has the majority voting rights in the company. - The extent to which there is common management and control between two or more alcohol manufacturers, or whether an alcohol manufacturer has the ability to influence the decision making of the other such that it is under an obligation to act, or can be reasonably expected to act, in accordance with its directions, instructions, or wishes.

- In the case where one or more alcohol manufacturers is a trustee of a trust, whether the terms of the trust deed govern who can control or influence the trustee (directly or indirectly) in respect of its decisions.

Economic independence

To determine whether manufacturers are economically independent from one another requires consideration of relevant arrangements. If one entity is economically reliant on the other (whether, for example, through direct monetary financing or reliance upon access to premises, equipment and other resources), then the two manufacturers will not be independent. Similarly, if two manufacturers are economically reliant upon the same third party to the degree that the third party is capable of exerting influence over both manufacturers, the independence test will be failed.

Factors that are relevant in determining whether alcohol manufacturers are economically independent from one another include:

- the nature of any financial arrangements between the alcohol manufacturers, including but not limited to inter-entity loans, subsidies, cost sharing or similar

- whether they share joint bank accounts or payment facilities

- any joint capital investments

- whether each alcohol manufacturer has

distinct manufacturing facilities

(whether owned or leased) and is not reliant upon any other alcohol manufacturer for the right to use and access those facilities.

Jointly owned or leased premises would not be considered distinct as one party could not act without consent of the other, or may be subject to the direction of the other.

Where an alcohol manufacturer leases premises and equipment from another alcohol manufacturer at an arm's length rate, it may satisfy the legal and economic independence requirement, subject to the terms and conditions of the commercial lease agreement (see Example 7J).

Where one manufacturer provides facilities to another manufacturer on an ad hoc informal basis, the requisite degree of independence is unlikely to exist as the second manufacturer's ability to carry on its business is subject to the ongoing agreement of the first manufacturer which could be terminated at any time. But where they have commercial lease arrangements in place that give the second manufacturer the certainty it needs to carry on its manufacture, the two manufacturers may still satisfy the economic independence test (in the absence of any other factors indicating the contrary). - Whether a manufacturer supervises and controls the production, testing and bottling of its own product without the other alcohol manufacturer being involved in these activities.

- Whether a manufacturer develops, labels and sells its own product and uses its own sales network without relying on the other alcohol manufacturer to undertake any of these activities on its behalf. Two manufacturers may still be considered independent even if they both engage the same advertising or marketing company to promote their products.

- Whether each alcohol manufacturer manages its own personnel (hiring, payment, performance management).

- Whether each alcohol manufacturer maintains separate accounting records and independently calculates and reports its excise and tax liabilities/entitlements . Two manufacturers may still be considered to be operating independently if they engage the same professional firm as long as the firm engages them under separate contracts of engagement and provides discrete services to each manufacturer that are billed and paid for separately.

Testing period

An alcohol manufacturer must be legally and economically independent of another manufacturer throughout the relevant test period. 185I

If the Remission Scheme applies:

- The alcohol manufacturers must be legally and economically independent of each other for the whole period between the day on which the financial year starts and the day on which a liability to excise duty arises on an alcoholic beverage that was entered for home consumption.

- Unless the remission of duty is made at the end of the financial year in which the alcoholic beverage was entered for home consumption - the alcohol manufacturer must have a reasonable expectation that those circumstances will exist for the remainder of the financial year .

If the Refund Scheme applies:

- Where the refund is claimed in the financial year after excise duty was paid , the alcohol manufacturers must be legally and economically independent of each other for the whole financial year in which the excise duty was paid .

- Where the refund is

claimed before the end of the financial year in which the excise duty was paid

- the alcohol manufacturers must be legally and economically independent of each other from the start of the financial year the duty was paid until the day the application is made , and

- the alcohol manufacturer must have a reasonable expectation that those circumstances will exist for the remainder of the financial year .

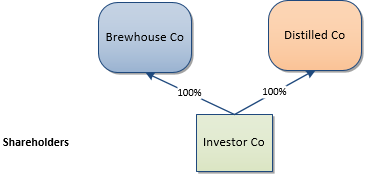

Example 7K

Brewhouse Co has an excise manufacturer licence to manufacture beer. Distilled Co has an excise manufacturer licence to manufacture spirits.

Investor Co owns 100% of the shares in both Brewhouse Co and Distilled Co.

Investor Co is a common controlling shareholder in both manufacturers. Where two or more alcohol manufacturers are directly or indirectly controlled by the same third entity, there is prima facie a lack of independence. Therefore only Brewhouse Co or Distilled Co (whichever claims first) can receive a remission or refund in a given financial year under the relevant Scheme (if it also satisfies the other eligibility criteria).

Example 7L

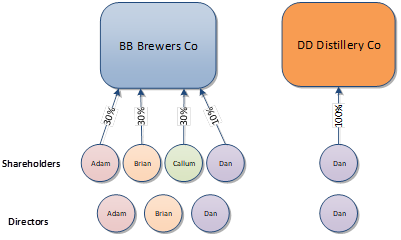

BB Brewers Co has an excise manufacturer licence to manufacture beer. DD Distillery Co has an excise manufacturer licence to manufacture spirits. The shareholding and directorships of the two entities are as follows:

All three directors of BB Brewers take an active part in the decision making of the company. All shares in BB Brewers carry equal rights.

The manufacturers have separate lease arrangements in place in respect of different parts of the same premises. Each manufacturer has the exclusive use of and control over the part of the premises they lease.

Each manufacturer is responsible for developing, manufacturing, packaging and storing its own alcoholic beverages. Each manufacturer employs and manages its own personnel. However, both manufacturers have engaged the same independent contractor to manage their accounting and tax reporting obligations. That contractor provides discrete services to each company and invoices them separately.

Each manufacturer maintains its own separate banking facilities and there are no intercompany loans or similar financial arrangements between them.

Whilst Dan is the sole shareholder and director of DD Distillery and therefore has control over its operations, he does not appear able to direct the decision making of BB Brewers Co (based on his minority shareholding and all three directors take an active part in the decision making).

The facts indicate that BB Brewers Co and DD Distillery Co have the capacity to make business decisions independently. They are therefore legally and economically independent of each other and both entities would be entitled to receive a remission or refund under the relevant scheme, subject to satisfying the remaining eligibility criteria.

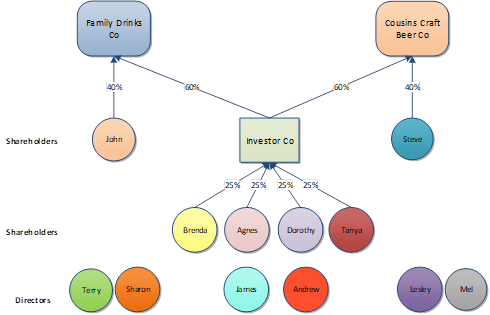

Example 7M

Family Drinks Co and Cousins Craft Beer Co are family run businesses. Family Drinks Co has an excise manufacturer licence to manufacture beer and spirits. Cousins Craft Beer Co has an excise manufacturer licence to manufacture beer.

The relevant shareholdings and directorships of each company are shown below. All shares in Family Drinks Co and Cousin Craft Beer Co carry equal rights. Brenda, Agnes, Dorothy and Tanya have equal shareholdings in Investor Co.

Both Family Drinks Co and Cousins Craft Beer Co have separate manufacturing, testing and bottling facilities and each develop their own products based on instruction from their own head brewer/distiller.

While operations of Family Drinks Co and Cousins Craft Beer Co appear to be independent (as they do not share facilities or have input into each other's products), Investor Co has a controlling interest (60%) in both companies and can therefore make decisions in respect of each company. That is, Investor Co is a common controlling shareholder. Prima facie, there is a lack of independence between the alcohol manufacturers. Therefore only Family Drinks Co or Cousins Craft Beer Co (whichever claims first) will be entitled to receive remissions or refunds under the relevant Scheme in a given financial year (if it also satisfies the remaining eligibility criteria).

Example 7N

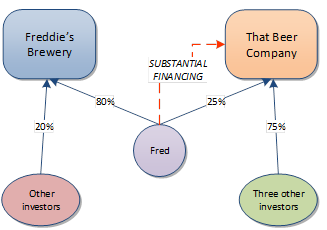

Freddie's Brewery and That Beer Company both have an excise manufacturer licence to manufacture beer. The shareholdings of the two entities are as follows:

All shares in Freddie's Brewery and That Beer Company carry equal rights. Fred has a controlling interest (80%) in Freddie's Brewery. Fred also has a minority interest (25%) in That Beer Company but has provided substantial financing to the company that it would struggle to obtain through external sources. Without the finance provided by Fred, That Beer Company would be incapable of carrying on its operations. The interest rate charged to That Beer Company and the repayment terms are at commercial rates.

Given the reliance That Beer Company has on Fred's finance to carry on its operations, Fred is able to exert influence over Board decisions. Accordingly, despite the fact Fred only has a minority shareholding in That Beer Company, and thus no common controlling shareholding exists between the two breweries, he is able to influence the business decisions of both manufacturers. While Fred's control of Freddie's Brewery is legal in nature (due to his controlling shareholding), and his control over That Beer Company is economic in nature (due to their reliance upon his financing), Fred is nevertheless able to exert control over both manufacturers. Therefore, the two breweries are not considered to be legally and economically independent of one another.

It is not necessary that Fred actually asserts influence over the operations of either brewery - the independence test is failed where Fred is capable of asserting influence over both breweries.

Example 7O

GG Distillery Co and Never First Distillery both have an excise manufacturer licence to manufacture spirits. No common controlling shareholders exist between the two entities.

Capital Bank is the chief lender to both distilleries, each of whom is reliant upon the bank to finance its activities. Without the finance from Capital Bank, neither distillery would be able to operate. Capital Bank does not have an equity interest in either distillery.

Notwithstanding the reliance of both distilleries upon the same bank lender, the mere fact the distilleries have obtained funding from the same bank will not point to a conclusion that they are not legally and economically independent.

Example 7P

Easy Drink Co owns a brewery complex and focuses its production on 'easy drinking' lagers suited to consumption in warm weather. During winter their trade shrinks and they have idle capacity in their plant.

Inventive Ales Pty Ltd is established by an acquaintance of the managing director of Easy Drink Co. Easy Drink Co wants to develop a 'winter beer' and devises a recipe and brand name which it owns. Easy Drink Co leases a portion of its brewery to Inventive Ales to enable the latter to manufacture the winter beer using Easy Drink's recipe. Inventive Ales manufactures the beer and under the terms of its agreement with Easy Drink Co, must sell the beer to Easy Drink Co at cost plus a markup. This is Inventive Ale's main activity and its profitability is dependent upon the agreement with Easy Drink Co.

While Inventive Ales has manufactured the beer, it is dependent upon Easy Drink Co for both its recipe and its market. It also has no ownership in the intellectual property so its very ability to sell the beer is dependent upon its arrangement with Easy Drink Co. Although the two manufacturers may be dealing with each other contractually on an arm's length basis, the economic reliance of Inventive Ales is so great that the two manufacturers would not satisfy the legal and economic independence requirement.

(c) Have you fermented or distilled at least 70% of the alcohol content of your alcoholic beverage?

You will only be eligible for a remission or refund if you fermented or distilled at least 70% by volume of the alcohol content of the beverage on which you had an excise liability (Remission Scheme) or on which you paid duty (Refund Scheme). 185J

While you must have fermented or distilled at least 70% of the alcohol in the final product, in the case of spirits, we will accept that you have distilled the alcohol where you purchase a base spirit, and re-distil it, with or without other ingredients. 185K

Provided you ferment or distil at least 70% of the alcohol content of the final alcoholic beverage, the remaining alcohol content in the final beverage can come from alcohol which you have not fermented or distilled, such as purchased spirits, or other alcoholic beverages.

Where you manufacture a product by merely blending purchased spirit with other ingredients, you will not be eligible for a remission or refund in respect of that product. For example, most domestically produced ready-to-drink beverages would not qualify as most of these products are produced from spirits that are imported in bulk, and then blended with soda.

Example 7R

Easy Drinks Co holds an excise manufacturer licence to manufacture other excisable beverages. It manufactures a popular ready-to-drink beverage called 'Vodka Chiller'. Easy Drinks Co sources vodka from a local supplier. Easy Drinks Co blends the vodka with other ingredients to produce the Vodka Chiller products and sells them to a retailer. Easy Drinks Co is liable for excise duty on the goods sold.

Whilst Easy Drinks Co is considered to be an alcohol manufacturer who manufactures an alcoholic beverage, it does not distil at least 70% of the alcohol content of the Vodka Chiller. As such, it does not satisfy this requirement and is not eligible to claim a remission or refund under the relevant Scheme.

(d) The 'still ownership test

If the remission or refund is in relation to a beverage that has been distilled, you must also satisfy all of the following 'still ownership tests' 185L :

- to have sole ownership of one or more stills that have a capacity of at least five litres

- at least one of those stills must be installed and ready to use at the beginning of the financial year, and

- at least one of the stills must have been used during the financial year for the purposes of manufacturing any alcoholic beverages.

However, you can disregard the 'still ownership test' if you are within your first two financial years of being eligible under the Remission Scheme or Refund Scheme (this refers to eligibility in general, not just in respect of distilled beverages).

Example 7S

An alcohol manufacturer received a remission of duty for beer it manufactured and entered for home consumption in each of the two previous financial years. In the current financial year, the alcohol manufacturer is seeking a remission of duty on gin. The manufacturer must meet the still ownership requirements in respect of any remission under the Remission Scheme for the gin as the manufacturer first became eligible to a remission under the Remission Scheme in the financial year two years prior to the current financial year.

It does not matter that the remissions in each of the previous two financial years were not in respect of a distilled beverage, nor would it matter if the licensed alcohol manufacturer did not receive a remission until the current financial year. The period prior to having to own a still commences in the first financial year in which the manufacturer could have received a remission and extends to the end of the following financial year. For example, if an entity first commenced manufacture of alcoholic beverages in May 2021, the period prior to having to own a still would end on 30 June 2022.

The outcome would be the same if the alcohol manufacturer had received refunds under the Refund Scheme rather than remissions, or a combination of the two in the financial year two years prior to the current financial year. The outcome would also be the same if the alcohol manufacturer had ceased to manufacture beer and enter it for home consumption after the first financial year.

7.3.4 WHEN CAN I APPLY FOR A DRAWBACK OF EXCISE DUTY?

You can apply for a drawback if you export alcohol products that have had excise duty paid on them. [186]

We will only pay a drawback if [187] :

- prior to the exportation, you advise us that you intend to claim a drawback (we can exempt you from this requirement, in writing, either on all claims for drawback or any particular claim. [188] )

- before exportation of the excisable alcohol products on which duty has been paid, the goods are available for inspection by us, and

- you keep records that show:

- that duty was paid on the alcohol products (for example, invoices), and

- the alcohol products were exported (for example, an export declaration number or bill of lading)

- you lodge a drawback claim in the approved form no later than 12 months after the alcohol products were exported

- the claim sets out the amount of the drawback and a statement that the goods have not been, or are not intended to be, re-landed in Australia, and

- the amount of the claim or an aggregate of the claims is at least $50.

The amount of the drawback will not exceed the amount of excise duty that was paid. [189]

Example 7T

A liquor distributor purchases a quantity of duty-paid beer and spirits which it supplies to an entity overseas.

The liquor distributor applies for a drawback of the duty component of the beer and spirits. To support the application, the company provides the ATO with copies of invoices of purchase and the bills of lading, which will include details of the export declaration notice (EDN) number.

7.3.5 WHAT HAPPENS IF I AM OVERPAID A REFUND OR DRAWBACK?

If we overpay you by way of a refund or drawback then you must pay the overpaid amount back. We can demand that you pay back the amount and if you do not repay the amount within the time we specify in the demand we can recover the amount through the courts as a debt due to the Commonwealth. [190]

7.3.6 WHEN ARE EXCISABLE ALCOHOL PRODUCTS EXEMPT FROM EXCISE DUTY?

Excisable alcohol products are exempt from duty if they are:

- exported

- sold for use as ship's or aircraft's stores [191]

- with our approval, delivered as small samples [192] , or

- subject to remission without application. [193]

What are ship's and aircraft's stores?

Ship's and aircraft's stores are goods for the use of passengers or crew on international journeys (for example, alcohol for sale to passengers on board a cruise liner).

There are limits on the quantities of excisable alcohol products that are not liable to excise duty as ship's stores [194] :

- alcoholic beverages (other than beer) must be sold to passengers or crew by the glass or nip.

If you supply ship's or aircraft's stores underbond , you must obtain a movement permission to move the goods from the licensed premises to the place of export.

Can I deliver samples without payment of duty?

Yes, you may be able to deliver small samples of excisable alcohol products without payment of duty and without entry. You must apply to us for approval to deliver any sample without the payment of duty. Your application must:

- be in writing

- specify who the sample is for

- specify the quantity for approval, and

- specify the purpose of the sample.

A small sample would normally consist of less than a saleable amount or an amount that is suitable for the purpose for which the sample is required; for example, testing and evaluation. Samples of product provided to customers in order to secure an order for that product (pre-delivery samples; that is, samples that arrive separately to the bulk goods), are not considered to be 'samples' that can be approved for delivery without the payment of duty.

|

| You do not include approved samples in your excise return ; however, you must keep records of any samples you deliver. |

To apply for approval, send your application to us via:

- the Online Services for Business

- write to us at

- Australian Taxation Office

- PO Box 3514

- ALBURY NSW 2640

7.4 PROCEDURES

7.4.1 HOW DO I APPLY FOR A REMISSION OR REFUND?

An application for a remission (excluding automatic remissions in clause 2 of Schedule 1) or a refund of excise duty must be submitted in writing. However, Schedule 1, subclause 1(1), paragraph (b) of the Excise Regulation provides that where a remission may be allowed and the goods have been totally lost or destroyed or otherwise ceased to exist an application is not required. Records to substantiate your claims must be maintained and produced when requested. [195]

An application for a refund must be lodged within 12 months after the day when the excise duty was paid for the following refund circumstances [196] :

- goods that, while subject to the CEO's control, has deteriorated, been damaged, pillaged, lost or destroyed, or become unfit for human consumption

- goods that, while subject to the CEO's control, are no longer worth the amount of duty paid on them

- duty was paid on goods through manifest error of fact or patent misconception of the law

- an alcohol manufacturer is eligible for a refund under the excise refund scheme for alcohol manufacturers.

For all other items listed in the table at clause 1 of Schedule 1 there is no time limit for lodging your application for refund. To ensure the excisable alcohol products do not find their way into the Australian domestic market we may wish to inspect or supervise the disposal of the goods. If underbond goods must be destroyed off site, you must apply for a movement permission to move them from the licensed premises to the place of destruction.

|

| Unless alcohol products have been accidentally destroyed, you should contact us before moving or destroying any that are subject to remission or refund. We will provide you with direction and advise if the goods are to be inspected or the destruction supervised. |

|

| For more information about movement permissions refer to Chapter 5 - Movement permissions . |

You can elect to have a refund credited to your excise account or paid directly into your bank account.

|

| To apply for a remission, send us a completed Excise remission (NAT 4289). You can use the Excise remission instructions to help you complete this form. |

To apply for a refund, send us a completed Excise refund (NAT 4288). You can use the Excise refund instructions to help you complete this form. Applications can also be made on company letterhead as long as all the relevant information is provided. |

If you are not satisfied with our decision to refuse your refund or remission, you can request a review of our decision by lodging an objection within 60 days.

|

| For more information about your review rights refer to Chapter 8 - Reviews and objections . |

7.4.2 HOW DO I APPLY FOR A DRAWBACK?

To apply for a drawback of duty, send us a completed Excise drawback (NAT 4287) or an application on your business letterhead. You can use the Excise drawback instructions to help you complete NAT 4287.

Your drawback application must be received not later than 12 months after the day on which the goods were exported. [197]

If we refuse to pay your drawback and you are not satisfied with our decision you can request a review of our decision by lodging an objection within 60 days.

|

| For more information about your review rights refer to Chapter 8 - Reviews and objections . |

7.4.3 WHAT DO I DO IF I NEED MORE INFORMATION?

If you need more information on remissions, refunds, drawbacks and exemptions contact us via:

- the Online Services for Business

- phone 1300 137 290

- email at alcohol@ato.gov.au , or

- write to us at

- Australian Taxation Office

- PO Box 3514

- ALBURY NSW 2640

We will ordinarily respond to electronic requests within 15 business days. We will ordinarily finalise private rulings within 28 days of receiving all necessary information. If we cannot respond within 28 days, we will contact you within 14 days to obtain more information or negotiate an extended response date.

7.5 WHAT PENALTIES CAN APPLY TO OFFENCES IN RELATION TO REMISSIONS, REFUNDS, DRAWBACKS AND EXEMPTIONS?

The following are the penalties that may apply after conviction for an offence.

Evade

If you evade payment of any duty which is payable, the maximum penalty is five times the amount of duty on the excisable alcohol products or where a court cannot determine the amount of that duty the penalty is a maximum of 500 units. [198]

False or misleading statements

If you make a false or misleading statement, or an omission from a statement in respect of duty payable on particular goods, to us, a penalty not exceeding the sum of 50 penalty units and twice the amount of duty payable on those goods. [199]

7.6 TERMS USED

Excisable alcohol products

Excisable goods are goods on which excise duty is imposed. Excise duty is imposed on goods that are listed in the Schedule to the Excise Tariff Act, or an Excise Tariff alteration, and manufactured in Australia.

As these guidelines deal with alcohol products, we have used the term excisable alcohol products.

Excisable alcohol products include:

- beer

- spirits

- premixed drinks known as ready-to-drink (RTD) beverages

- brewed beverages that are not beer, and

- high strength spirit for non-beverage use, including denatured spirit.

Excise control

Goods are subject to excise control from the point of manufacture until they have been delivered into the Australian domestic market or for export.

Goods subject to excise control cannot be moved, altered or interfered with except as authorised by the Excise Act.

Excise return

An excise return [200] is the document that you use to advise us:

- the volume of excisable alcohol products that you have delivered into the Australian domestic market during the period designated on your PSP, or

- the volume of excisable alcohol products that you wish to deliver into the Australian domestic market following approval.

Penalty units

Refer to section 4AA of the Crimes Act 1914 for the current value of a penalty unit.

Underbond

This is an expression not found in excise legislation but it is widely used to describe goods that are subject to excise control. Excisable goods that are subject to the Commissioner's control are commonly referred to as 'underbond goods' or as being 'underbond'. This includes goods that have not yet been delivered into the Australian domestic market and goods moving between premises under a movement permission.

7.7 LEGISLATION (quick reference guide)

In this chapter we have referred to the following legislation:

Section 24 - Excisable goods and goods liable to duties of Customs may be used in manufacturing excisable goods

Section 58 - Entry for home consumption etc.

Section 61A - Permission to remove goods that are subject to CEO's control

Section 64 - Delivery of samples free of duty

Section 78 - Remissions, rebates and refunds

Section 79 - Drawbacks

Section 80 - Recovery of overpayments of refunds, rebates, and drawbacks

Section 120 - Offences

Section 160A - Ship's stores and aircraft's stores

Section 10 - Application for remission, rebate or refund of excise duty

Section 11 - Period for making an application for refund or rebate of excise duty

Section 12 - Amount of remission, rebate or refund of excise duty

Section 14 - Drawback of excise duty on goods

Section 15 - When drawback of excise duty is not payable

Section 16 - Conditions relating to drawback of excise duty - general

Clause 1 of Schedule 1- Circumstances in which remission, rebate or refund may be made on application

Clause 2 of Schedule 1 - Circumstances in which remission, rebate or refund may be made without application

Section 4AA - Penalty units

Section 46 - What is a subsidiary

Latest update

25 February 2022

| Section | Changes and updates |

| Example 7J | Updated to correct current practice that a taxpayer must apply for a new license for each additional premise they intend to manufacture goods. |

| Date: | Version: | |

| 1 July 2013 | Original document | |

| 1 July 2015 | Updated document | |

| 7 September 2017 | Updated document | |

| 21 February 2018 | Updated document | |

| 5 August 2019 | Updated document | |

| 4 June 2021 | Updated document | |

| 9 July 2021 | Updated document | |

| 23 December 2021 | Updated document | |

| 25 February 2022 | Updated document | |

| You are here | 1 July 2024 | Current document |